Info from:

http://hes.lbl.gov/hes/makingithappen/financing.html

EEMs or

EIMs

Financing

an Energy Home Improvement

If you're thinking of refinancing your home to pay for your

remodel, or you want to buy a house and fix it up, you can get an

energy-efficient mortgage (EEM) to cover the costs of energy upgrades.

These mortgages let you roll the cost of those improvements into your home

loan. With a really well-designed EEM, you end up not spending a cent for

the energy measures. There are EEMs for remodeling (in some areas these

are called energy improvement mortgages, or EIMs) and others for

purchasing houses that are already considered energy efficient. The latter

allows homebuyers to qualify for more house with less income because

utility bills will be low. If you are remodeling your home with the

intention of selling it, remember energy efficiency adds value. You can

get an EEM to do the upgrades, then sell your home at a higher price to a

buyer who is taking advantage of an EEM to buy an energy-efficient home!

Who Offers EEMs?

Currently EEMs are secured by a variety of sources

including two government agencies: the Department of Housing and Urban

Development's Federal Housing Authority (FHA), and the Department of

Veterans Affairs (DVA). Also, private secondary mortgage lenders,

including the Federal National Mortgage Association (Fannie Mae) and the

Federal Home Loan Mortgage Corporation (Freddie Mac) also offer EEMS.

Countrywide Home Loans, Inc., Norwest Mortgage, Inc., and GMAC Mortgage

Corp. are among the independent mortgage companies (they guarantee the

loan themselves rather than selling it to a secondary lender) that are

getting into the act. There are many differences between the various

loans, not the least of which is who qualifies. But the basic principles

are the same.

How EEMs Work

EEMs are added on to your regular mortgage. They allow you

to make cost-effective improvements which will save you more each month on

your utility bill than the cost they add to your monthly mortgage payment.

The government-sponsored loans have several special benefits. First, they

let you add on the money for the improvements to your mortgage even if

this means you exceed traditional loan limits. Second, you don't have to

qualify for the additional money. Third, and probably most important, 100%

of the cost of the improvements can be financed. Since all improvements

must be cost effective to qualify, this means there are no out of pocket

expenses. Your mortgage payments go up a little, but your utility bills go

down more. You can even realize a positive cash flow. It's like getting

paid for improving your home.

The private sector's secondary lenders (they buy loans from

the primary lender such as your local bank) have been slower to accept

EEMs, but this is changing. Fannie Mae and Freddie Mac are offering EEMs

in more and more states. The requirements are a bit different. For

example, these conventional lenders do not allow loan limits to be

exceeded, and they require borrowers to qualify for any additional money.

But even a private market EEM will save you money and improve your home.

And in some states there is an added benefit. Borrowers may

have the opportunity to qualify for a larger loan with a lower income

through what is called a 2% stretch of the qualifying ratios. Lenders

consider the lower utility bills you will have, and then allow you a

higher mortgage accordingly. (This is not available everywhere, but is

worth asking about.)

More Financial Options

In addition to energy mortgages, there are many other loans

available to help pay for your energy upgrades. Some are traditional home

improvement loans. Others, specifically designed for energy-efficient

retrofits, have added benefits such as lower interest rates. And for

low-income home owners, there may be loans with very low to no interest,

or other special benefits.

Loans are usually offered at the local level through

partnerships of utilities, banks, secondary lenders, and non-profit

conservation groups. There are also loans offered at the federal level,

but ultimately these are doled out locally through state agencies and

local utilities. Some loans may require a home energy rating; others do

not. Energy loans may run as low as a few hundred dollars or up into the

tens of thousands of dollars.

One useful HUD/FHA loan offered nationwide is the Title 1

home improvement loan. Homeowners may borrow up to $25,000 for general

home improvements including, but not limited to, energy upgrades.

Another is HUD's 203(k) loan to purchase a home in need of

repair or modernization. Under this program you can get one mortgage loan,

at a long-term fixed or adjustable rate, to finance both the acquisition

and the rehabilitation of the property. The local HUD field office in your

area can provide more information on these loans.

Dollar limits for energy

loans are generally lower than for traditional home improvement loans, but

so are the interest rates. Using an energy loan to supplement a home

improvement loan could help reduce overall interest rates and could help

you afford more efficient retrofits.

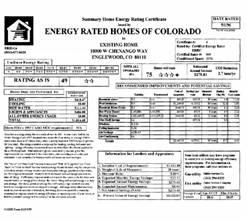

In the case of loans secured by the government, $200 of the

cost of the rating may be financed (as long as overall loan limits are not

exceeded). Ratings currently range in cost from around $100 to $350 and

average about $200.

Other Raters.

Some loans require the HERS rating but others allow for alternative energy

audits performed by appraisers or energy consultants. Such audits will

give the same type of information to the lender. In all cases it's best to

check with your lender first to know exactly what is required.

Appraisals.

For loans secured through the private mortgage market (non-government

loans), an appraisal is sometimes required. This will usually depend on

the state you're living in. In some states, Fannie Mae and Freddie Mac now

accept a HERS rating instead of an appraisal. In other states they still

require an appraisal showing an increase in your home's value that's equal

to the cost of the improvements. Due to the special nature of energy

improvements, which bring lower utility bills and increased comfort, such

an increase in appraised value is generally accepted in the industry. If

you need an appraiser, be sure to find one who understands the value of

energy improvements and is willing to do the extra work involved in

filling out the forms required by the private mortgage industry.

Choosing Your Improvements

In order for an improvement to qualify for an EEM it must

be deemed "cost-effective" (except in the case of some DVA loans). This

means two things. The monthly savings on your utility bills that are

generated by the improvement must be greater than the added monthly cost

of the energy mortgage; and over the lifetime of the improvement, your

total savings must be greater than your total costs--including

maintainance costs--by at least one dollar. Cost-effectiveness is

determined by the energy rating.

In some cases, an improvement that is not found to be

cost-effective may be financed if all your improvements as a package pass

the cost/savings test.

Getting the Loan:

Steps to an

EEM

Once you have a home energy rating, or some other

acceptable documentation, and you know what improvements you want, you're

ready to apply for your loan. An energy mortgage cannot be added after the

loan is granted, so be sure to apply for the EEM and your mortgage at the

same time.

The process of getting an EEM is fairly straight-forward.

But understanding the details, requirements, and benefits of the many

different types of loans is not. At the application stage (if not before)

you may want to see if there's someone in your area who can help you

facilitate the process. Many HERS providers act as facilitators

themselves, or can point you toward someone else who can do the job. A

facilitator handles the nitty gritty details, making sure all your papers

are filed on time, and easing the work for both you and your lender.

If there is not a facilitator near you, you will have to do

a little extra work to make sure you have all of the up-to-date

information on the different types of loans, the benefits, and the

requirements for your area. The EEM industry is rapidly growing and

changing, and there are many local variations to the loans. For advice,

contact one or more of the organizations listed at the end of this

chapter.

Doing the Work

After the loan goes through there is a limited amount of

time for the energy improvements to be made, usually between 90 and 180

days depending on who is securing the loan. Money for the improvements is

held by the bank in an escrow holdback account until the remodel is

complete. Then it is paid to the contractor or homeowner. Since the

improvements are already chosen when the loan application is made, and a

contractor may be found before the loan is granted, 90 days is usually

more than enough time to complete a retrofit. Most contractors will finish

the job before receiving payment, so the escrow holdback does not create

any problems.

Home improvement loans traditionally require that 150% of

the estimated cost of the remodel be set aside by the bank in an escrow

holdback account. This guards against cost overruns, but can be an

inconvenience. But with most energy improvement mortgages only 100%, the

actual projected cost of the remodel, is held back.

If you decide to do the work yourself, make sure you leave

enough time to complete the project in the designated time frame. In the

case of do-it-yourself remodels, the underwriter may only grant an energy

loan for the cost of materials.

Examples

Energy loans vary quite a bit. Here is what one might look

like:

A local utility joins with a bank to offer energy loans

with below-market interest rates. If you are a customer of the utility you

may borrow up to $25,000 for a high-efficiency heat pump, an

energy-efficient water heater, insulation improvements, and duct repairs.

Interest rates on loans are tiered

·

up to $5000 @ 6%

·

$5000-$10,000 @ 8%

·

$10,000-$18,000 @ 10%

·

$18,000-$25,000 @ 12%.

Another

example:

Mike

and Debbie Brown decided to buy the house they had been renting for five

years using an EEM. They added $3,250 onto their base mortgage to cover

weatherization and other energy improvements. All the costs of the energy

improvements were paid for through the FHA mortgage, including the cost of

the energy rating, so there were no out-of-pocket expenses. The

improvements were installed as soon as the loan went through. The Brown's

mortgage increased by $21.61 a month to cover the energy upgrades. But

their utility bills dropped by over $90 a month, leaving them an extra

$720 a year. And they own a more valuable house that's comfortable year

round.

|

Cost Savings with an

Energy-Efficient Mortgage

Compare the monthly housing costs of a remodeling EEM against

those of a standard loan, both secured through the Federal

Housing Authority.

|

Loan-Related Expense |

Standard Loan |

EEM |

|

|

|

|

|

Purchase Price |

$100,000 |

$100,000 |

|

Cost of Energy Improvements

|

n/a |

4,000 |

|

Adjusted Purchase Price |

100,000 |

104,000 |

|

Mortgage Loan Amount 100%

|

100,000 |

104,000 |

|

Monthly Principal Interest

|

730 |

759 |

|

Monthly Taxes and Insurance

|

150 |

150 |

|

Total Monthly Mortgage |

880 |

909 |

|

Monthly Utilities |

126 |

71 |

|

Total Monthly Housing Expense

|

1006 |

980 |

Benefits to the Homeowner:

·

$26 per month net savings

·

$312 per year net savings

·

A more comfortable, more valuable home at no extra cost

|

|

Getting the Information You Need

To find what's offered in your area, start with your local

utility. Other places to look are the field office of the federal Housing

and Urban Development (HUD) agency, your state energy office, and any

local energy conservation groups. For mortgages, try the local field

offices for the various mortgage companies and organizations listed in

this chapter or the HERS contacts listed below.

It can take a good bit of sleuthing to snoop out money for

grants and loans, and the process can be frustrating, but give it a try.

It can also pay to read the literature that comes with your utility bill,

the stuff most of us promptly throw away. Often it describes energy

financing opportunities in your area.

Take the time to call more than one of the contacts listed

as no organization is guaranteed to have all the complete and up-to-date

information.

Resources

Berko, Robert L. Consumers Guide to Home Repair Grants

and Subsidized Loans. South Orange, NJ: Consumer Education Research

Center, 1996.

Energy Rated Homes of

America (RESNET)

12350 Industry Way, Suite 208

Anchorage, AK 99515

Phone: 907-345-1930

E-Mail:

resnet@corecom.net

WWW:

http://www.natresnet.org/RESNET.htm

Home Energy Rating Systems

(HERS) Council

1511 K St., NW, Suite 600

Washington, DC 20005

Phone: 202-638-3700 ext.202

E-Mail:

HERS@aecnet.com

WWW:

http://www.hers-council.org

US Department of Energy

Office of BTS, EE-40

1000 Independence Ave., SW

Washington, DC 20585-0121

Phone: 202-586-7819

E-Mail:

John.Reese@hq.doe.gov

WWW:

http://www.doe.gov

US Environmental Protection

Agency

ENERGY STAR Homes Program

401 M St., SW, MC 6202J

Washington, DC 20460

Phone: 888-STAR-YES

WWW:

http://www.epa.gov/energystar_dat.html